When it comes to life lessons, teaching your children how to maintain good credit is one of the important ones. Proper credit can help your child land a job, buy a place to live and save money over and over again. In addition to teaching your child what he or she needs to do in order to earn solid credit scores, it is also worthwhile to teach your children about the credit mistakes that need to be avoided.

Mistake #1: Not Paying Attention

Too many Americans are in the bad habit of ignoring their credit reports and scores. Even people who work hard to keep their credit healthy can be guilty of this mistake. Just because you believe that you have made all of your payments on time and that you do not have any outstanding, defaulted debts doesn’t mean that you can ignore your credit reports. Credit reporting errors occur every day.

While credit reporting is not your responsibility, it is up to you to ensure that the information contained in your credit reports is accurate. Nobody is going to do this for you.

Checking credit reports quarterly or, better yet, monthly is the best practice for protecting the health of your credit. This is a habit which you will want to teach your child to develop as well. Think of how often you check your bank statements and then copy that frequency with your credit reports.

Mistake #2: Overspending

Overspending can lead to a lot of different credit problems, especially when you overspend on credit cards. It is important to teach your children to only charge what they can afford to pay off on a monthly basis, not only for financial purposes like avoiding interest fees, but also to protect their credit scores.

When you charge more than you can afford and revolve an outstanding credit card balance on your credit reports, your credit scores can suffer. This is true even if your monthly credit card payment is consistently made on time, a fact which many people do not understand.

In fact, about a third of the points in your FICO and VantageScore credit scores are based on the relationship between your credit card limits and account balances. The lower your credit card utilization, the better. Teach your kids how to use credit right the first time.

Mistake #3: Co-Signing

Another mistake you should teach your children to avoid is co-signing, even for loved ones. When you co-sign, you are equally liable for the debt, just as much as you would be if you were the sole borrower or account holder. The account will show up on your credit reports and could damage your scores even if all of the payments are made on time.

Additionally, the indebtedness will be counted against you whenever you apply for new financing of your own, making it harder for you to qualify for new loans or accounts on multiple levels. Teach your child to always maintain credit independence and make sure that you lead by example when it comes to this very important lesson.

Mistake #4: Late Payments

It goes without saying that late payments and good credit scores do not mix. Many people, however, fail to understand that even the occasional late payment can potentially wreak havoc upon their credit scores.

Over a third of the points in your scores are based on the “Payment History” category of your credit reports. In order for your child to be equipped to earn and maintain good credit, he or she must understand that late payments need to be 100% off limits, 100% of the time.

You probably know the basics when it comes to earning good credit, or at the very least you probably understand the concept that you need to pay your bills on time in order to achieve good credit scores.

Yet making on-time payments is not going to be enough if you want to achieve credit score greatness. Credit scoring is actually quite a bit more complicated than that.

In today’s world, however, that’s simply not enough. And if you are monitoring your credit scores on a monthly basis, you may feel confused as to why they’re not higher, especially if you are making a deliberate effort to improve them. Sadly, the reason your credit scores are a disappointment is not always so obvious.

Here are five reasons why your credit scores might be lower than you wish.

Reason #1: Your Credit Card Utilization Is High

Most people do not realize that how you manage your credit card debt is nearly as important to your credit scores as the payment history on your accounts. FICO and VantageScore, in fact, are designed to base 30% of your credit score points on your debt, and much of that 30% is based on your credit card balances relative to your credit card limits.

The “Revolving Utilization Ratio” is the term which describes the relationship between your credit card limits and your credit card balances (as they appear on your credit reports). If your credit reports show accounts which are highly utilized (meaning you have tapped into a sizable percentage of your available credit limits), your scores will likely suffer even if you make every single payment by the due date.

Reason #2: You Applied for Too Much Credit Recently

Another factor which credit scoring models consider when calculating your credit scores is how often you have applied for new credit within the past 12 months. Higher numbers of applications can be indicative of elevated credit risk. As a result, if you want your credit scores to soar, then you should probably try to keep new credit applications to a minimum moving forward.

Reason #3: You Have a Poor Mix of Account Types

Credit scoring models also reward consumers who demonstrate that they have experience managing a variety of different account types. If your credit reports only contain a single type of account, such as credit cards, then opening a small installment account such as a credit builder loan could be helpful. Of course, making your payments by the due date and keeping a $0 credit card balance on your reports is more important than your account mixture, but account mixture still matters nonetheless.

Reason #4: You Believe Occasional Late Payments Are Acceptable

Some people mistakenly believe that the occasional payment slip up is not a big deal, especially if the majority of the time they make their payments as agreed. Unfortunately, that is not the way credit scoring works. A credit scoring model will look at your credit reports and search to see if any late payments are present. If the answer to that question is yes, then you will probably be awarded fewer credit score points than you would have earned otherwise.

Reason #5: You Open New Accounts Too Often

The age of your oldest account and the average age of the accounts which appear on your credit reports are two more factors which credit scoring models like FICO and VantageScore look at whenever your scores are calculated. As your average age of accounts grows older, your credit scores will generally benefit. However, if you are constantly opening new accounts then you do not give that average account age a chance to increase, a habit which could hold your credit scores back.

Think about the amount of time you spend commuting to work. What about the times you spend thinking about your office work. What about your colleagues; some who you hate spending your days with? What about your ‘horrible’ boss? What about that sales target or deadline you have to hit?

Now, think about the reasons why you do all these? Essentially, you do all these because you want a better life for you and your family. You are not alone.

We all want the same things in life. Happy families, good health, and excellent emotional well-being. That is the reason why we struggle every day.

Now, after making your money, you want to enjoy it in peace. Sadly, most Americans are not achieving this. Recent studies show that while wages in America are improving, albeit slowly, many people are still living paycheck to paycheck. Statistics also show that more than 43 million of Americans are in food stamps. All this is a clear indication of a population that is struggling.

To achieve financial freedom no matter the amount of money you make, budgeting is very important. On paper, this topic seems easy but in the real world, it is really tough.

How many times have you created a budget only to forget about it within days? I believe that we have all been through this process in the past.

In this article, I will explain a few tips on how I achieved the goal of creating a budget and sticking with it.

Start with your net income

The first step is to forget your gross income and focus on the net income. The net income is simply the amount of money that you get after all the deductions. If you work only one job, then this is the amount you should put down. If you have other side jobs like freelancing, you should also include the net amount you get in this part.

Set a Budget Plan

Many budget plans have been developed but the one I really like (and use) is the 50/30/20 budget. In this plan, you allocate your money in three ways. The first 50% of your net income goes to the necessities, while the 30% goes to wants, and the rest goes to savings and debt repayment.

Needs

Necessities are the things you must use every month. They include items like rent, food, school fees for your children, transport, and utilities like internet and cable TV.

Since necessities are your biggest income-spenders, I recommend that you only opt for things you can afford or those that are reasonably priced.

For example, you don’t need to live in a fancy 3-bedroom apartment if you are just two family members. You don’t have to pay the top-tier cable service if you don’t watch all the TV channels. You don’t need to drive to work every day if an Uber is cheaper. Also, you don’t have to pay for the fastest internet subscription if you don’t use internet as much. While you love your children a lot, you don’t have to take them to the most expensive school, in the neighborhood.

Simple tweaks like that will save you a lot of money in the long term.

Wants

Wants are simply the things you can do without. For example, we all love going out to dinner or ordering a meal kit service. Also, most of us have a desire to drink a good bottle of wine. We also love going out to a trip.

There is nothing wrong in indulging in such activities. In fact, since you are the one who works so hard to make the money, you need to enjoy it.

The caveat is this. Your wants should always be 20% (or less) of your net income. Overspending on the wants has led many people – like Johnny Depp – to struggle financially later in their lives.

Savings and debt repayments

“A SIMPLE FACT THAT IS HARD TO LEARN IS THAT THE TIME TO SAVE MONEY IS WHEN YOU HAVE SOME.” -JOE MOORE

Finally, the remaining 30% should go to savings and servicing of the debt.

Like I mentioned, most Americans are living from paycheck to paycheck which makes it hard for them to save money. If you follow this plan, this should never be the case.

If like me you have debts – like mortgages and car loans – you should pay for them using the remaining 30% of your income. On debts, always consider the following:

Always, check for loans with the lowest interest rates.

Always check for the small hidden charges in these loans.

Always pay them on time. This will help you improve your credit rating.

After paying the debt, you should save the rest of the money. When saving, you should consider saving for the short term and saving for the retirement. This is because you want to be financially secure now, and also when you retire.

When saving for retirement, you should ensure that you start early in life. The chart below provides a better explanation on why starting early will always pay off.

When saving, I recommend that you set some money aside for emergencies. Think about this. What would you do if your home was affected by the recent hurricanes or the California fires? An emergency fund can help you in this.

The Hard Part

Now that you have created a budget, the hard part will be sticking with it. This will not be easy. Believe me. I have been there before.

A few tips will help you achieve this.

1. Always record your transactions. A good way to achieve this is by using mobile apps like Mint and Personal Capital that track your spending and present your income and expenses in a dashboard.

2. Always assess your spending on a regular basis. This could be weekly, monthly, quarterly, or even annually.

3. Always remember to unsubscribe to services you don’t need. If you no longer care about Wall Street Journal, Netflix, Plated, and Adobe, just unsubscribe from their services.

4. If need be, please talk to a certified financial planner who will provide you with a roadmap to achieve your financial goals.

5. Have a person to check up on you. This could be your wife, sibling, or a close friend.

The goal of a budget is not to make you live a dull life. Its goal is not to restrict you from having fun and enjoying your money. Its goal is to give you a holistic and long-term view about your financial health. In fact, you will have a tough future if you ignore the three parts of the budget.

The negative mark of a collection on your credit reports can have a severe impact on your scores. Unfortunately, anyone who tries to do the right thing and pay a collection account off, quickly realizes that the account being marked as “Paid” on their credit, did not really help improve their scores.

It seems everything involved with credit reporting tends to be slighted against the American consumer. Rather than rewarding you for paying off debt, your scores drop when you do so, and if you pay off a collection account, full payment will not result in the removal of the negative mark.

One thing consumers have turned to in an effort to ensure that a collection account will be removed after payment, is to request a “pay for deletion.” This is where the consumer asks the debt collector if they will they will delete the tradeline from the consumer’s credit report, in exchange for payment.

However, this practice is expressly against the rules set out by the Consumer Data Industry Association (CDIA) guidelines, and some argue that it undermines the credit system.

The CDIA is the voice of the consumer reporting industry, representing consumer reporting agencies including the nationwide credit bureaus, regional and specialized credit bureaus, background check companies, and others. Their primary function is to assist data furnishers (such as banks, credit unions, consumer credit card companies, retailers, and auto finance companies) in using the standard electronic data reporting format called the Metro 2® format that the credit reporting industry has adopted.

What the CDIA is NOT, is a federally regulated entity that must comply with the Fair Credit Reporting Act (FCRA). Thus, it is just an established standard of reporting for lenders or credit issuers to follow when reporting consumer credit activities to the various credit reporting agencies or credit bureaus.

Arguably, there are some who are adamantly against this “pay to delete” practice saying that it compromises the integrity of the credit scoring system by making it extremely harmful to parties who rely on such information in making lending decisions. Once these tradelines are deleted there is NO record anywhere of that charged off account.

So, what does the Fair Credit Reporting Act (FCRA) say? The law specifically states that creditors who furnish information about consumers to consumer reporting agencies must:

Provide accurate information, which includes the duties to: correct and update information; provide notice of dispute or closed accounts; provide notice of delinquency of accounts; and provide notice of identity theft-related information

Inform consumers about negative information which will be or already has been furnished to a reporting agency (no later than 30 days after furnishing).

Investigate certain disputes submitted directly by consumers.

What the FCRA doesn’t say, has been said by the courts.

”…the industry guidelines—such as Metro 2—do not establish the standards for accuracy under the FCRA. Florence v. Cenlar Fed. Sav. & Loan Case No.: 2:16-cv-0587-GMN-NJK (D. Nev. Mar. 1, 2018)”

“…Ms. Mestayer has failed to point to any authority indicating that a failure to comply with an industry standard is a failure to comply with the law. Furthermore, other courts have rejected an attempt to rely on the Metro 2 standard. See, e.g., Mortimer, 2013 U.S. Dist. LEXIS 51877, at *32-33”

“As pled, Defendant’s alleged noncompliance with the Metro 2 Format is an insufficient basis to state a claim under the FCRA. Mortimer v. Bank of Am., N.A. Case No.: C-12-01959 JCS (N.D. Cal. Apr. 10, 2013)”

Clearly, the reporting standard holds no water when used as a legal reason to state a claim when a violation has occurred. So why would an industry created standard that has no legal foundation within the Fair Credit Reporting Act make it so difficult for consumers to successfully have their “pay to delete” requests approved?

The answer to that remains unknown though there are certain collection agencies who are now accepting “pay to delete” requests even though they go against the CDIA “rules” that other collection agencies are still following.

The FCRA does grant the Bureau of Consumer Financial Protection (BCFP) both enforcement and rulemaking authority in connection with those it supervises, which would include debt buyers and debt collectors, and many — but not all — data furnishers.

So the BCFP could address this policy if it chose to. Until then, the battle for American consumers to get that second chance, by doing the right thing and paying debts owned by collections agencies, will continue. But maybe now they have some new information to use in their fight.

What this three-digit number means and why it’s so important to your financial future.

Your credit score is a three-digit rating that tells potential lenders and financial institutions how much risk is associated with lending to you.

Scores typically range from 300-850; the higher the score, the lower the risk. The first time I ever saw my credit score was at the request of my soon-to-be landlord.

I had never been asked for a credit report before, and I had no idea what it would say. Luckily, my parents had encouraged me to sign up for a credit card when I was in college so that I could start to ‘build credit’ – a term that made zero sense to me at the time but an absolute necessity to ever register in the eyes of potential creditors.

It seemed counter-intuitive that by spending money on credit, I became a more desirable candidate for a lease, a mortgage, or even additional credit. But that’s exactly how it works. Using your credit card and paying those bills (and others) on time paints a picture of a financially responsible person.

I was pleasantly surprised by my credit score, but that isn’t always the case. For those who haven’t established a credit history, there isn’t enough information to generate an accurate rating, which can be just as detrimental as having a poor credit score.

What’s Considered ‘Good’ and ‘Poor’ Credit and Why It Matters

Your credit score, which ranges from 300-850, is not set in stone. So, if you’re currently sitting with a poor credit rating, don’t despair! It will continue to fluctuate throughout your life, and I’ve included some tips for improving your score in the coming sections.

Typically, any rating below 650 is considered poor, and ratings 700 and up are considered good. Having poor credit means that you’re less likely to be approved for a loan and that any mortgage you’re able to secure will come with higher interest rates than for those with good credit scores.

Building up a good credit history means that financial institutions see you as a minimal-risk investment, which gives you access to the lowest interest rates and better terms. A good credit score can make all the difference in obtaining a loan, renting an apartment and saving you money on interest payments.

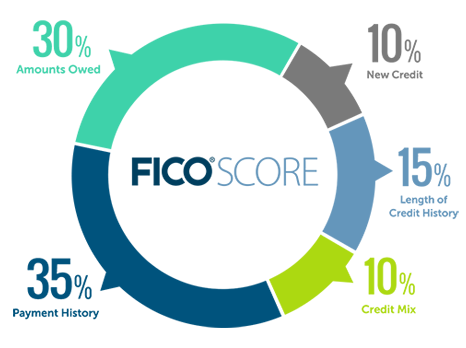

How It’s Calculated

Your credit score is determined by five main categories, listed below by order of importance:

Payment History: Have you paid your bills on time? This is the most important factor in calculating your overall score. If you’re consistently paying your credit card bill on time (at least the minimum monthly amount) as well as all your other bills, that’s going to go a long way in establishing a good credit score.

Utilization Ratio: What percentage of available credit are you using? If you’re reaching the limit of credit available to you, it may reflect negatively on your score.

Length of Credit History: You need at least 2 years of recent history for an accurate credit score, but the longer, the better.

Types of Credit: If you have a credit card, line of credit and mortgage, they will all be included in your assessment. It can help to have positive experiences with different types of credit.

New Credit: Opening multiple new credit accounts in a short period of time can raise red flags and bring down your credit score.

How to Improve It

So, now that we all know the benefits of having a good credit score, how can we make sure to get one? Here are six tips for improving your credit score:

Tip #1: Get a Credit Card

If you don’t have a credit card, apply for one ASAP! Without a credit card to pay off each month, credit bureaus will have a hard time tracking your financial habits. You need to build that history.

Tip #2: Watch the Spending

Yes, it’s important to spend money on your credit card(s). But, it’s just as important to stay as far away from the credit limit as possible. Try to set an imaginary limit of 50% or less. So, if your card has a limit of $10,000, pretend it’s $5,000. Better yet, pretend it’s $1,000 and pay it off every month.

Tip #3: Increase Your Credit Limit

If Tip #2 is proving to be a challenge, you might want to consider increasing your credit limit. Using a lower percentage (less than 50%) of the total credit available to you is one of the fastest ways to improve your credit score. Note: Opening a bunch of new credit cards will not have the same effect!

Tip #4: Pay on Time

Pay all your bills on time! Missing even one payment can have an impact on your credit score, so set up reminders or automated payments to ensure you’re never late. Aim to pay off your credit card bill in full every month but if that’s not possible, paying more than the minimum monthly amount will help to improve your credit score.

Tip #5: Don’t Close Your Accounts

If you’ve paid off a credit card, you might be tempted to close it. Don’t. Keep it around for your monthly phone bill or other utilities. Closing any credit account erases all the history associated with it, and it reduces the total credit available to you – which messes with your ‘Utilization Ratio.’

Tip #6: Monitor Your Credit Score

There are 3 major credit reporting agencies as listed by the government (link to https://www.usa.gov/credit-reports) where you can obtain your credit report. Try to check your credit once a year to monitor your score and flag any errors that could be negatively affecting your rating.

The Bottom Line

None of us likes being reduced to just a number, but when it comes to finances, these three digits are quite often the first (and sometimes the only) thing that potential lenders will see when they look at you. So, find out where you stand and, if necessary, take the steps necessary to improve your credit score.

In life, you will make many decisions. You will select your career, your marriage partner, your preferred state to live, your preferred car to drive, and your home.

The latter decision is very important because of the initial costs involved and how it can influence your lifestyle.

In the United States, house prices have been on an upward trajectory with the median house price in the country being more than $200,000. This amount is unaffordable to many people.

This is where mortgages come in. Mortgages help people acquire houses and pay in small monthly installments. Today, more than 80% of all Americans have debt, and from these, 44% of them have mortgage debt.

Below, I highlight some of the best online mortgage lenders you can try.

Rocket Mortgage

Rocket Mortgage is an online-only mortgage provider from Quicken Loans. It is one of the biggest providers of mortgage providers in the country. In 2016, the company funded more than $7 billion in closed loans. If it was an independent company, Rocket Mortgage would rank among the top 30 mortgage providers in the country.

Using Rocket Mortgage, customers fill their data on its web or mobile platforms and then receive their approval within minutes. During the application, the customer does not use any paperwork whatsoever because the process is automated.

To apply for a Rocket Mortgage, you first need to create an account and then answer a few questions about yourself. Then, you should connect your bank accounts to the account you just created and then fill a few questions that are required by law. After answering all questions, Rocket Mortgage will give you several options for paying for the house so that you can select the one appropriate for you.

This process can take less than 20 minutes to complete.

Rocket Mortgage offers fixed-rate loans of between 8 to 30 years with ARMs of 5/1, 7/1, or 10/1. It accepts anyone with a minimum credit score of 620.

SoFi Mortgage

SoFi (Social Finance) is an online-only company that gives people a platform to borrow, invest, and insure.

The company’s online mortgage services allow people to borrow money by paying 10% of the home value and then paying the rest in installments. In application, the company analyzes the customer’s FICO scores and consider other factors like professional history, career prospects, income, and other factors like bill payments.

To apply for a mortgage with SoFi, you first enter your details on this page. Then, you should enter basic information like your state, whether you are buying or refinancing the house, your marital status, and whether you have another home. Such simple details.

Then, on the next page, you will be asked to enter your purchase price, down payment amount, and the amount you are borrowing. Finally, the platform will show you the rate quotes which you will select.

After this, you will wait for approximately 28 days before you know your fate.

The benefits of SoFi are that it considers non-traditional credit history, an average closing period of 28 days, it has no origination and application fee, and it offers flexible down payments that range between 10% and 50%.

The only challenge with SoFi is that it requires a minimum loan amount of $100,000.

Lenda

Lenda is a relatively new company in this space but one of my favorites. The company offers online mortgages and refinancing services.

To apply for a mortgage with Lenda, all you need to do is to answer several questions on this page for prequalification.

Then, on the next page, you will be given several options which you are supposed to select the one that matches your liking. Then, the Lenda suggestion engine will use its algorithms to see whether there are inputs you can enter to reduce your payments. Then, you enter several details, check your credit score, and then attach documents.

The entire process takes less than ten minutes, and the loan is processed within 36 days.

The pros of Lenda is that: there are no paperwork, fast processing period, the Lenda suggestion engine can save you money, cheap, and transparent.

The only problem with using the service is that it currently operates in five states (California, Colorado, Oregon, Texas, and Washington).

PennyMac

PennyMac is a public company started in 2008. The company offers customers mortgage and refinancing services online.

To get a mortgage with the firm, all you need to do is visit the website and answer a few questions about yourself. Then, PennyMac will give you a quotation page where you can select your preferred option or adjust your inputs to get a better deal.

Among the benefits of using PennyMac is that it offers government loans like FHA, USDA, and VA loans. Also, it has 15 locations where customers can be assisted. Also, it is offered across all states, and it has no minimum income requirement.

The only problem with PennyMac is that it charges origination fees and its loan calculator is usually not accurate because of the many assumptions it makes.

Better

Better was started in 2014 after its founder went through hell finding a good mortgage. Better aims to be the best mortgage and refinancing provider in the country by making the borrowing process transparent and fast.

To apply for a mortgage with Better, you are required to follow a few steps. First, you need to get pre-approved by answering a few questions, a process that takes about three minutes. After answering the questions, the verification process will take 24 hours or less. Then, you will be presented with a few flexible options for you to select from. Finally, you will be required to complete the application process.

The key pros of using better are faster loan closing of 10 days, getting an estimate within 3 minutes, transparent, support staff are not paid using commissions, a low deposit of 3% of the house, and an offer within 24 hours.

The only problem with Better is that it offers its services to several states including Arizona, Georgia, California, Illinois, Washington, Pennsylvania, Oregon, New Jersey, North Carolina, District of Columbia, Connecticut, and Colorado.

PNC Financial

PNC Mortgages is a product of PNC Financial Group, a Pittsburg based company with more than $366 billion in assets. The company operates more than 2,500 branches in the country where customers can get mortgages.

However, customers can also use its website to get any of its 5 types of mortgages which include: jumbo, fixed rate, adjustable rate mortgage, FHA, and VA loans.

To get a loan, all you need to do is visit this page and select the type of loan you want. Then, after filing the information on this page, you should wait for the bank to contact you within 1 to 2 days with more information.

The pros of using this company is that information on rates is readily available and that it has a large network of branches where you can get help from.

The problems with it are that the application process is not entirely online.

Final Thoughts

Applying for a mortgage can be hectic. From the paperwork to the determined sales executive looking to make a sale, to the cost, and to the lines in the bank. No one loves that.

Applying for a mortgage or refinancing online is an essential way of saving you money, time, and energy. That is why I recommend any of the companies I mentioned.

But, before you apply, ensure that you understand the type of mortgage you are applying to. Is it a fixed rate or variable? Ask those questions or do the research yourself. Also, make sure you read the terms and conditions page to get more details about the loan.

It’s no secret that a person’s social life can be incredibly expensive. From eating out and drinks to transportation and clothing, you can watch your bank account dwindle as you try to keep up with social events in your area.

If you live in a large metropolitan area like I do then you’re constantly being tempted with events, new restaurants, parties and even work functions. There isn’t a single day that goes by that there isn’t something going on in Miami, and I learned the hard way how much money it was costing me to keep up with the party scene.

Fortunately, there are multiple ways that you can save money without being a hermit. Here are some of the ways you can save a lot of money on being social, backed by personal experience.

Use Facebook to Keep an Eye on Free Events Near You

Facebook is a very cool tool for helping you keep an eye on free and low-cost events in your area. More specifically, Facebook tends to notify you of local events your friends and colleagues are interested in. If you actually look at the event pages, you’ll start to notice that many of the events are either free or cheap – especially if it’s some sort of promotion like a grand opening.

By actually paying attention to the Events tab on Facebook I have ended up at free parties, gotten free massages and scored coupons for restaurants.

Try Meetups

Meetups are usually free events filled with people of similar interests. You can meet at a coffee shop, go to a networking event or find free workouts depending on what you’re into.

The easiest way to find meetups is to go to Meetup.com and search for your interests. Just keep in mind that not all meetups are cost effective. For example, there’s a meetup in my area for young professionals once a week. It’s free to get into the party, but I’d still have to pay for alcohol and food which means that, unless I don’t drink or eat, my bank account would take a hit. On the other hand, a free yoga class in the park wouldn’t really cost me anything but an Uber pool ride.

Eat before going out

One of the best ways to save money on social events is to avoid buying food. You can do this by making sure you eat something before you leave. By the time you get to your friends you’ll be full and it’ll be easier to turn down buying food.

Enjoy nights in with friends

Because I grew up in a place like Miami, there’s this assumption that in order to have fun you need to go to a bar or a club. This is fine if you don’t mind spending $10+ on a watered down drink.

Once my friends and I got a bit older we actually just started hanging out at each other’s places. We’d watch movies or a game, order a pizza and split the cost. This has turned out to be way more cost effective – and actually more fun – than going out to a club.

Final Thoughts

Saving money doesn’t mean you need to be a social recluse and avoid having fun. There are plenty of ways to have fun, enjoy your friends and explore events in your town without breaking the bank

If you’ve ever read Robert Kiyosaki’s book, Rich Dad, Poor Dad, (one of the best selling business books of all time) you know one of his key themes in the book is about letting your money work for you.

Here are six easy ways to achieve this without having to break your bank account.

Buy One Bitcoin and Forget It

What does this chart make you feel?

If you didn’t get into bitcoin early enough, this chart is heartbreaking. I get that.

The good news is, according to some very. smart. people. it is nowhere near too late to get into bitcoin.

The simplest way in, is for you to buy one bitcoin and forget it. Here is the reason.

In Bitcoin, there are two sides. There are those people – like Jamie Dimon – who believe that bitcoin is a bubble that will eventually collapse under its own weight.

On the other hand, there are people who believe that bitcoin is worth much more. Wences Casares – a director at PayPal – believes that Bitcoin could even get to $1 million.

So, if you buy one bitcoin today, it will cost you about $5,600. If Jamie Dimon’s fears become true, the biggest loss you will make will be your initial $7,200. However, if Wences’ argument becomes true, your $7,200 will turn to $1 million without you doing anything.

“But wait Jay! I don’t have $7200 to invest right now!”

That’s ok! because you don’t have to buy a whole Bitcoin: “Just like all fiat currencies can be broken down into cents, 1 BTC can be broken down into smaller units all the way to eight decimal places: 0.00000001 BTC”

Using the same argument, you can also create a diversified portfolio of cryptocurrencies like Ethereum, Ripple, and Dash which are examples of some of the “alternate” cryptocurrencies available on exchanges like Bittrex.

If you’re looking to buy Bitcoin the easiest place to get started is Coinbase.com

But before you do, make sure you understand how to keep your cryptocurrency safe from hackers and thieves.

IMPORTANT: Investing in cryptocurrencies is extremely risky, and the markets are currently very loosely regulated. Do your own due diligence and research before investing in anything.

Invest in Real Estate

It won’t cost you much. Believe me.

Traditionally, to invest in real estate, you needed to have two crucial things: prime land, and money. A lot of it. You also needed to go through a bureaucratic process, from one office to another.

Today, you don’t need to do any of that. This is because technology has made it easy for anyone to invest in assets that were hard to do in the past.

Several platforms that help people pull resources together to build a building have been developed. My favorite one is a company called Fundrise which pioneered the model.

Using FundRise, investors from all United States can contribute as little as $500 each to develop a piece of land and watch their investment grow.

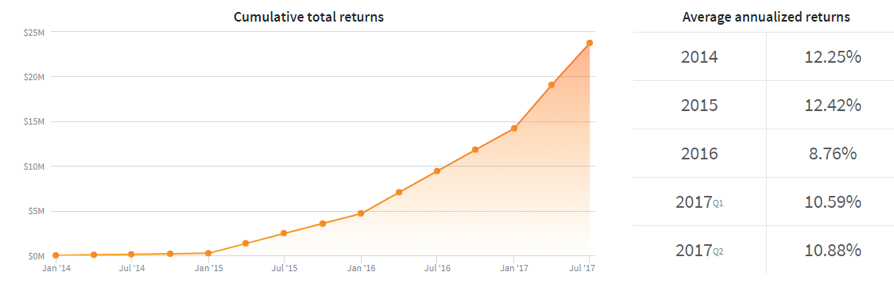

Already, the company has received and invested more than $1.4 billion in private real estate deals. The company has also attracted more than $55 million of venture capital.

Returns have been good too as you can see.

Quick Tips

Before you invest in Fundrise, you should compare it with other similar companies which include: Realty Mogul, Realty Shares, Patch of Land, and PeerStreet.

You can even diversify your money across several similar companies.

Do you due diligence by ensuring the company you invest with does what it says it does. See whether it is regulated. You don’t want to be in another Madoff-like situation.

Give Loans to People and Businesses

Again, this seems like a really difficult thing to do. How will you find the people or companies to lend money to? How will you evaluate them? What will you do if they default?

Truth is, all this is not hard. (In the past, it was)

This is because there are many technology-powered companies that makes all this very easy that you can do it within minutes.

One of my favorite platforms in this is LendingClub, a company listed in the New York Stocks Exchange.

The idea behind these peer to peer market places is simple. People and businesses are in need of capital and banks can be hectic. So, they make it easy for businesses and people to get the funds that they need without having to go to a bank. As an investor, you earn interest the same way banks do.

Using the platform, you can invest as little as $25 and see your money grow.

What’s better? You are not alone. Many American banks – who feel threatened by these companies – also provide their capital to them.

LendingClub is not the only company offering these services. There are others like Prosper, SoFi, Upstart, and OnDeck among others.

Using these platforms, you can make between 4% to 10% returns per year.

Quick tip.

Before you invest in a peer-to-peer marketplace, please do your research. I also recommend that you invest in P2P companies that are public like LendingClub, OnDeck, and Prosper. This is because these companies are mandated by law to release several disclosure documents. They also offer investor conference calls where they are asked questions that might be of interest to you.

Invest in Startups

Startups are disrupting all sectors in the United States. Uber has disrupted the traditional taxi businesses. Airbnb is disrupting the hotel industry while Tesla is disrupting the vehicle industry.

For these startups to grow, they need capital. A lot of it.

This is where you get in. Using technology, you can be a venture capitalist like Chris Sacca and Bill Gurley of Benchmark even when you don’t have a lot of money.

Companies like SeedInvest, MicroVentures, and WeFunder offer platforms that let you invest in vetted, early and late-stage companies with as little as $100.

These companies remove three main bottlenecks for ordinary investors. First, they find companies that have the potential of succeeding. Second, they enable investors to pool capital and invest in one company. This means that you don’t need to have a lot of money to invest in the next Facebook. Third, they let you track how your investment is doing.

To me, MicroVentures is the best of the three platforms. Its past investments include companies like Facebook, Twitter, and Pinterest among others.

Remember that not all startups you back will succeed. In fact, in all venture capital firms, the investments that don’t work are usually more than those that work out fine.

For example, a seasoned group of investors like KPCB and Throve Capital invested more than $118 million in a juicing company called Juicero. After launching its $400 juicer, Juicero was shut down after Bloomberg exposed the company for creating a product that was not needed.

Another good example is Theranos which had raised about $686 million and got to a valuation of $9 billion before it was exposed for being a fraud.

To succeed in all this, you need to conduct intensive research on companies you want to invest in and diversify your portfolio among many quality companies.

Automate Your Investments

You’ve probably seen the lavish lifestyle showcased by top hedge fund managers.

Truth is, hedge funds have a broken fee system that allows them to make money even when they don’t perform well. They take 2% of the assets and then take a 20% incentive fee from the profits they generate. Therefore, a hedge fund manager with $10 billion in assets under management, is sure of making $200 million a year.

In addition, not all of us can afford investing in a hedge fund because mostly they serve high-net worth investors and pension funds.

This is where robo-advisors come in.

Robo-advisors are firms that take money from individual and allocate them in diversified portfolios based on the individual’s risk appetite. Good thing about these advisors is that they don’t charge people a lot of money and you can invest as little as $10.

Some of the best robo-advisors are Motif Investing, WealthSimple, Wealthfront, Betterment, and Ellevest among others.

Today, these platforms have raised hundreds of millions of dollars from venture capital firms. In return, they have raised billions of dollars from investors.

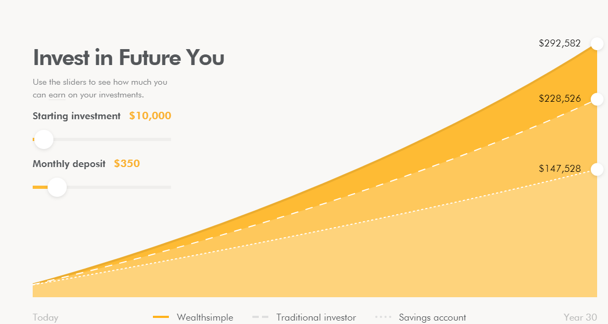

Consider the chart below from WealthSimple.

Please note.

These companies are significantly new in the industry. They have not been tried and tested especially in difficult market environment. Therefore, diversify your funds across several companies and do your due diligence before you put your money in any of the company.

Also, in robo-advisors, you should consider companies like Acorns that bring an interesting angle in investing. Acorns – and several other companies – allow you to invest your spare change. For example, if you had $50 and you decide to buy a dress worth $45, Acorns allows you to invest the $5. If you make this a habit, in a long time, you will start seeing your money grow.

ETFs

Do you want to invest in the stock market but don’t have the time or expertise to do so? If the answer is yes, a low-cost ETF can be a good option for you.

To many, an ETF is a jargon but in reality, it is a very simple concept. An ETF is an asset class that tracks a basket of stocks, commodities, or even currencies. For example, an ETF like the VanEck Vectors Gold Miners ETF (GDX) tracks the movement of companies that mine gold.

Investing in ETFs is different from investing in individual stocks because of its diversification. This means that by buying an ETF like GDX, you are buying a diversified group of companies.

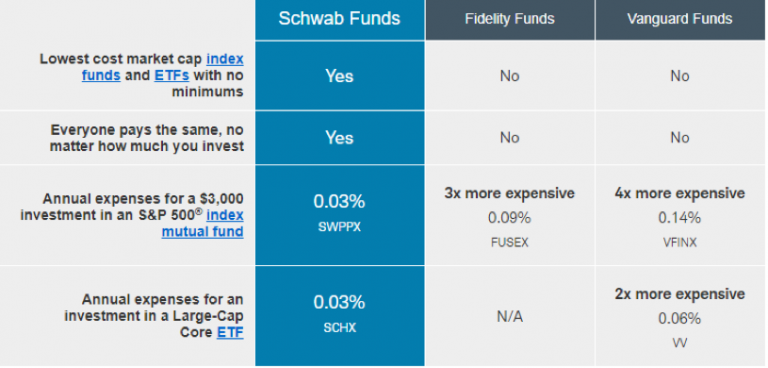

You can buy ETFs from your traditional broker like Charles Schwabb and Fidelity.

However, technology has made it possible for you to bypass the fees that these traditional companies charge. As shown below, the fees can be huge.

You can bypass these fees by using modern brokerage firms like Robinhood and Stash. Robinhood charges no fees per trade while Stash charges investors a monthly fixed fee of $5.

The unique thing about the platforms and strategies I have shared above is that they don’t need you to spend a lot of money. Also, after investing, you will not need to do anything apart from tracking your investment.

Your credit score is probably the most important thing in your financial life. This is because it tells the lenders your credit worthiness. A bad credit score – below 600 – can mean limited or expensive sources of funds when you need them the most.

This situation is particularly worse for people who have declared bankruptcy before. If you have, the bankruptcy issue can haunt your credit score for years.

Fortunately, many financial institutions offer quality credit cards for people with bad credit. Here are five of the best credit cards for you if your credit scores are low

Indigo Platinum card

If you have a bad credit score – and filed for bankruptcy before – the Indigo Platinum Card is an ideal card. The card comes with a low annual fee that ranges from $0 to $99 and an annual interest rate of 23.9% for purchases and 29.9% for cash advances.

The card offers no fees for cash advances for the first year. After one year, the card charges you either $5 or 5% of the transaction.

In addition to the physical card, the providers (Genesis Bank) provides you with access to a mobile-friendly platform where you can access the information in your card.

Also, the card gives you the ability to shop in more than 35 million locations worldwide.

Finally, the card does not require a security deposit from you.

Signing up for the card is easy. First, I recommend that you take time to read the terms and conditions for the card which are available in this page.

After this, you should select the design of your card and then provide a few details about yourself in this page and then proceed for pre-qualification. Then, you will proceed to make the full application.

Caution

The card comes with a penalty of not more than $38 for late repayment, overlimit, and return payments. It also comes with more penalties which you can read in the terms and conditions page.

Total Visa Credit Card

The Total Visa Card is ideal for people with bad credit who want to access funds and improve their credit rating. The card is offered by Mid America Bank & Trust Company.

The card is easy to get. All you need to do is visit the website, select your card design, and then answer a few questions for pre-qualification purposes. In all, the process can take less than five minutes to complete.

The card charges an APR of 29.9% for purchases and advances.

It comes with a few charges which include: $89 one-time processing fee, $75 annual fee for the first year which drops to $48, and no monthly fee for the first year which increases to $75 in the following year.

Finally, it requires no cash advance fee for the first year which increases to either $5 or 5% of the money you borrow.

The card also charges a penalty of $38 for late repayment or for returned payment.

Another limitation for the card is that it requires one to have a checking account. Also, you can only shop with it only in the United States.

Quick note

It is very important for you to read the terms and conditions before you subscribe to any credit card. For the Total Visa Card, you can find the terms here

Milestone Gold MasterCard

The Milestone Gold Mastercard is provided by the Mid America Bank & Trust Company. It is ideal for people with poor credit score even those who have declared bankruptcy before.

The card offers features like:

Easy process to enroll for the card. You can apply for the card online within minutes. However, you will be required to pay a registration fee of $5.

Fast pre-qualification without impact to your credit score.

A low APR of 23.9% for purchases and 29.9% for advances.

A low annual fee of $75 in the first year and $99 thereafter.

It comes with the Mastercard Gold Benefits which include: Master Rental Insurance, Extended Warranty Coverage, Master Roadassist Service, and Travel Assistance Services.

You can buy with it in more than 35 million locations worldwide.

Free custom card design

An online platform to access your credit card account.

The card comes with several fees and penalties which you must always consider when enrolling for a credit card.

It charges you a fee of up to $38 for late payment, overlimit, or returned payments. Also, it charges you a 1% fee for all foreign transactions. For the first year, it charges you no fee for cash advances which increases to either $5 or 5% per transaction.

First Access Card

This is another card ideal for people with bad credit score. It is provided by the FDIC-insured bank, Mid America Bank & Trust Company.

The card’s features are:

An APR of 29.9% for purchases and cash advances.

Monthly reports to the major credit reporting agencies.

A simple, fast, and secure online application. To register, you need to visit this website and fill in your details. It takes less than a minute to get approved.

No processing fee for the first year which rises to $89 thereafter.

No cash advance fee for the first year.

The card’s limitations are: you can’t purchase items when outside the United States, and you can’t select the card design of your choice.

You should also consider the different fees that the card comes with which include: a monthly fee, annual fee, cash advance fee, late payment fee, returned payment fee, copying fee, and the express delivery fee.

Final Thoughts

No one choses to have a bad credit score. When it happens, you need not to give up. As you have seen, there are companies that offer credit to people like you.

The secret is to work towards improving your score. You can achieve this by paying your credit debt early and to pay all the fees on time.

Another mistake you should avoid is getting a credit card without reading the terms and conditions. Some cards come with so many hidden fees that could lead to worsening of your credit score.

Saving money is always a good thing, especially when it comes to your grocery bill. Whether you are feeding a family of four or setting just a table for one, groceries can add up fast. We gathered up some tips for you to make the most of your next trip to the supermarket of your choice.

Make a Grocery List

Creating a list of what you need at the grocery store does two main things for you. First, it allows you to get all of the items you need without forgetting what it is you came to shop for in the first place. Second, you will buy less impulsively if you stick to only what you need. Grocery stores make sure to try and get you to buy the latest and greatest of something through end cap displays and store samples.

Try the Store Brand Items

Believe it or not, there are times when store name brands and popular name brands items are manufactured in the same place! These are usually the same item with just different packaging. Simply check the ingredients on the packaging to compare. Using the store brand items can save you money while not sacrificing taste.

Don’t go to the Store When you are Hungry

In our fast-paced lives, we tend to run around and do errands before we have time to eat. Studies show that going to the grocery store hungry creates the desire for more food than you need. Do your best to shop on the weekends when you have more control over when you eat and can shop when your tummy is not on empty.

Avoid the Aisles in the Center of the Store

Essential Items are placed around the perimeter of grocery stores, like dairy, meat, and vegetables. This creates the need to go through some aisles to get to what you want to obtain. So if you are in a hurry try to skip the middle aisle where the stores know they can get you with items you didn’t intend on buying.

Use Those Coupons

Saving even 20 cents here and there can really add up to some serious savings. If you don’t receive it in the mail, you can usually find your store’s circular in the front of the store. More often than not, it not only lists the specials of the week but has a few coupons to use as well. And of course, there is always the Sunday paper coupons that can usually help make a dent in your bill.

Eye Level is Sometimes Deceiving

When deciding on that next marinara sauce, make sure you look above and below your eyesight – that’s where the higher priced items are placed. Just because you see it first, doesn’t mean it’s the best deal. Often you will find the more inexpensive versions, not at eye level. This is the same reason that items appealing to kids are at their eye level.

Eat When Produce is in Season

Want to get the best deal on produce? Make sure you buy fruits and vegetables when they are in season. Buying these items out of season is not only costly but sometimes means they come from other countries. Not to mention they taste way better when picked fresh and at peak flavor.

Steer Away from Convenience Foods

From pre-cut and –washed salads to sliced up fruit, the more convenient the food is in preparation, the more likely it’s going to cost higher than doing it yourself. It only takes a few minutes to slice and dice these foods and then store them in your own containers so you can grab them easily on the go.

These are just some basic ways to save but highly effective if you utilize them on a daily or weekly basis. It’s for the most part about discipline and wanting to watch that final cost be as low as possible. Simply implement a few tactics each time you go grocery shopping and watch the savings start to be routine.